Title Insurance: A Historical Financial Safeguard

Property ownership has always carried inherent risks, from boundary disputes in colonial America to fraud schemes during the Gilded Age. The development of title insurance in the mid-19th century represented a pivotal innovation in financial risk management, transforming how Americans approached real estate transactions. Understanding this protective mechanism through a historical lens reveals not only its current importance but also the market forces that shaped its evolution. For investors, journalists, and students of financial history, examining title insurance offers valuable insights into how the industry adapted to economic crises, regulatory changes, and technological advancement.

The Origins and Purpose of Title Insurance

The concept of title insurance emerged from a fundamental problem in property transactions. When buyers purchase real estate, they need assurance that the seller actually owns the property and has the legal right to transfer it. According to the Florida Office of Insurance Regulation, this form of insurance protects property owners and lenders against financial loss from defects in a property's title.

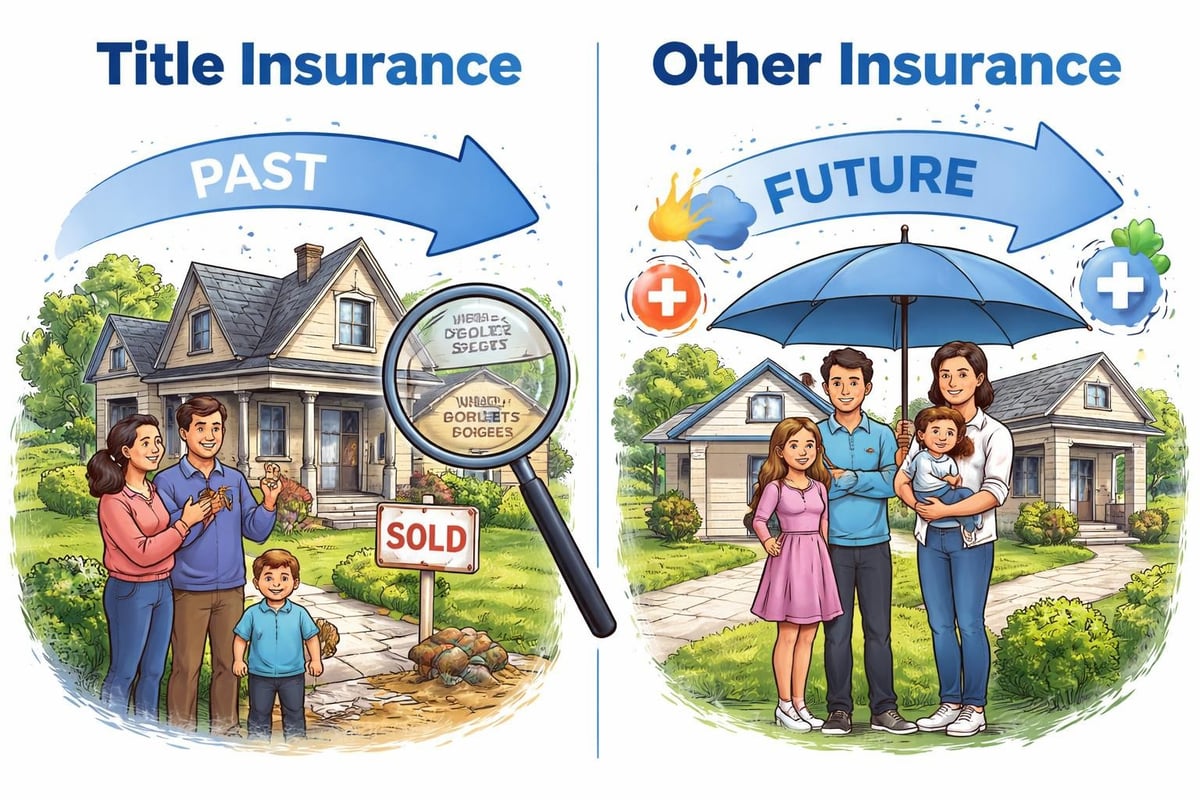

Unlike other insurance types that protect against future events, title insurance uniquely guards against past occurrences. The policy covers issues that existed before the purchase date but were unknown at closing. This backward-looking nature distinguishes it from homeowners insurance or liability coverage, which address future risks.

Historical Context of Property Rights Protection

The American title insurance industry traces its roots to 1876 Philadelphia, where a Pennsylvania Supreme Court decision sparked the creation of the first title insurance company. Before this innovation, property buyers relied on attorneys' opinions about title validity. When lawyers made errors, buyers had limited recourse beyond suing the attorney, often an unsatisfactory remedy.

The Office of Public Insurance Counsel in Texas explains that title insurance emerged as a more reliable solution, creating a financial backstop when title defects surfaced. This development paralleled other late 19th-century financial innovations, including the expansion of commercial paper markets and standardized securities.

Major economic downturns throughout American history revealed the value of this protection. During the Great Depression, countless property owners faced foreclosure proceedings that uncovered title irregularities. Those with title insurance found themselves better positioned to resolve disputes, while uninsured owners often lost properties entirely.

How Title Insurance Functions in Modern Markets

The mechanics of title insurance involve several distinct stages, each designed to identify and mitigate risk before policies are issued. The process begins with a comprehensive title search, examining public records for liens, encumbrances, easements, and other potential problems.

The Title Search and Examination Process

Professional title examiners review decades of property records, including:

- Deeds and conveyances documenting ownership transfers

- Court records revealing judgments or pending litigation

- Tax records showing unpaid property taxes

- Probate files confirming proper estate settlement

- Marriage and divorce records affecting property rights

The California Department of Insurance notes that this exhaustive research aims to identify issues before closing, allowing parties to address problems proactively. When searches reveal defects, transactions can pause while sellers cure the problems or buyers negotiate adjusted terms.

Following the search, underwriters assess risk and determine whether to issue a policy. This evaluation considers the property's history, transaction structure, and regional factors affecting title validity. The underwriting decision reflects accumulated industry knowledge about common defects and emerging risks in specific markets.

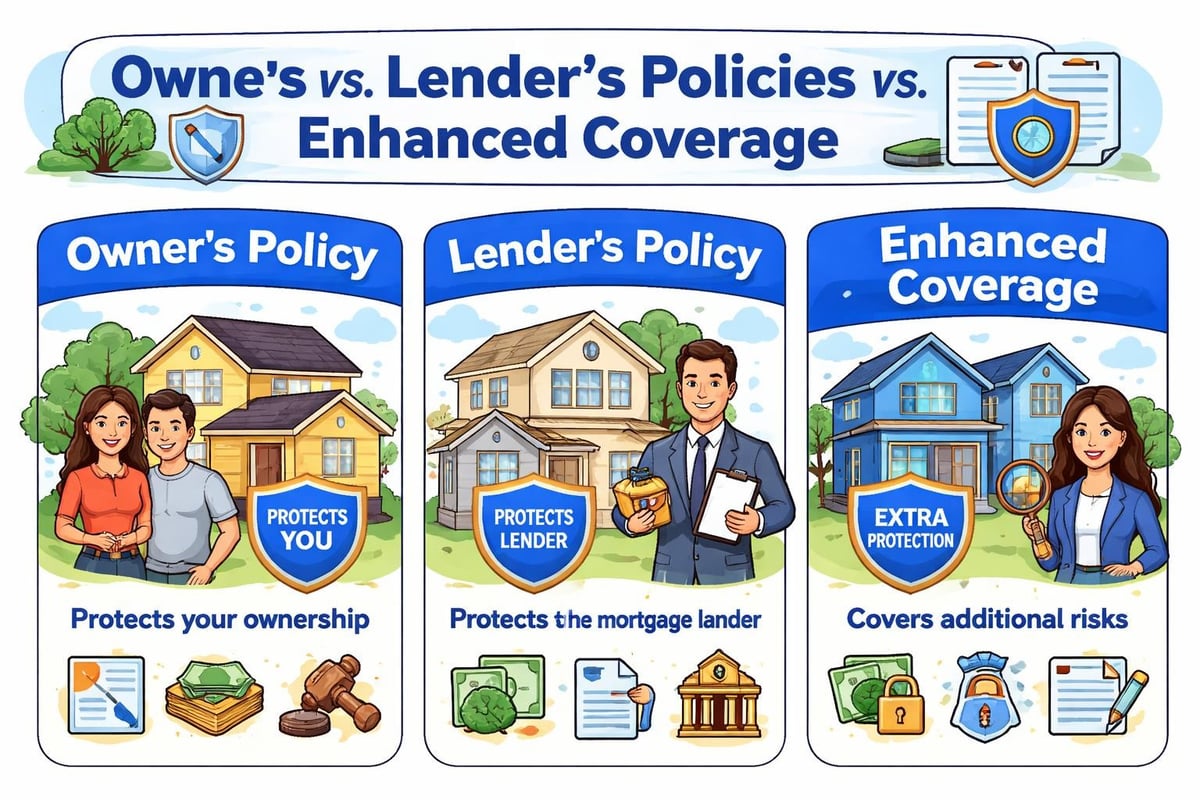

Types of Title Insurance Policies

Two primary policy types serve different stakeholders in real estate transactions:

| Policy Type | Protected Party | Coverage Duration | Typical Cost Basis |

|---|---|---|---|

| Owner's Policy | Property buyer | Until ownership ends | Purchase price |

| Lender's Policy | Mortgage lender | Until loan payoff | Loan amount |

| Enhanced Owner's | Property buyer | Until ownership ends | Purchase price plus extras |

The Virginia State Corporation Commission emphasizes that lender's policies protect only the lending institution, not the property owner. Buyers seeking personal protection must purchase separate owner's policies, though lenders universally require lender's coverage as a loan condition.

Enhanced policies emerged in recent decades, offering expanded coverage beyond standard protections. These policies may address issues like post-policy forgery, forced removal of structures due to permit violations, or enhanced access rights. The additional premium typically ranges from 10% to 30% above standard policy costs.

Historical Market Evolution and Industry Trends

The title insurance industry has experienced significant transformation across economic cycles. The National Mortgage News reported that title insurers generated $16.2 billion in premiums during 2024, representing a 7% annual increase driven by robust refinancing activity and sustained home sales despite elevated interest rates.

Industry Performance Through Economic Cycles

Historical patterns reveal strong correlations between title insurance premiums and real estate transaction volumes. During the 2008 financial crisis, industry revenues contracted sharply as home sales plummeted and foreclosures dominated market activity. The subsequent recovery demonstrated the sector's resilience, with premiums rebounding as housing markets stabilized.

Examining these patterns alongside other financial metrics provides valuable context for understanding broader economic health. Title insurance revenue often serves as a leading indicator of real estate market strength, offering insights into consumer confidence and lending activity.

The industry structure has also evolved considerably. While thousands of small, regional companies once dominated the market, consolidation has created several large national underwriters controlling substantial market share. This concentration affects pricing, service delivery, and technological innovation across the sector.

Regulatory Frameworks and Consumer Protection

State insurance regulators oversee title insurance, creating varied requirements across jurisdictions. The National Association of Insurance Commissioners coordinates among states to develop model regulations, though implementation varies significantly by region.

Some states employ rate regulation, requiring insurers to file premium schedules with regulatory authorities. Others allow competitive pricing within certain parameters. These approaches reflect different philosophies about market efficiency and consumer protection, similar to debates around price ceilings in other sectors.

Florida, Texas, and New York maintain particularly stringent regulatory oversight, including promulgated rate structures that limit insurer flexibility. Other states adopt more market-oriented approaches, permitting insurers to compete on price and service quality.

Common Title Defects and Coverage Scenarios

Title insurance addresses numerous potential problems that could cloud property ownership. Understanding these risks illuminates why this protection remains essential despite thorough pre-closing examinations.

Frequently Covered Title Issues

The Land Title Association of Mississippi identifies common defects that title insurance protects against:

- Forged documents in the property's chain of title

- Undisclosed heirs claiming ownership rights

- Recording errors in public records

- Fraudulent impersonation of property owners

- Mistakes in title examinations or legal descriptions

Each scenario carries financial implications that could exceed the property's value. A forged deed from decades earlier, if undetected, might invalidate all subsequent transfers. Without title insurance, current owners would bear the costs of litigation and potential ownership loss.

Historical examples abound of title defects surfacing years after transactions closed. In one notable case, a property sold multiple times over three decades before heirs of an earlier owner proved their ancestor's signature had been forged. The title insurance company defended the current owner's rights and ultimately settled with the claimants, preserving the policyholder's ownership.

Exclusions and Limitations

Like all insurance products, title policies contain exclusions limiting coverage. Standard policies typically exclude:

- Defects created by the policyholder after closing

- Issues disclosed in the title commitment but not remedied

- Governmental regulations affecting property use

- Environmental contamination

- Native American land claims in certain jurisdictions

Understanding these limitations helps property buyers make informed decisions about purchasing enhanced coverage or accepting certain risks. The Florida Department of Financial Services provides guidance on evaluating coverage options and understanding policy terms.

Technology and Future Industry Directions

The title insurance sector faces significant technological disruption as digital tools transform traditional workflows. Industry leaders are betting on technology and efficiency to navigate market pressures, regulatory shifts, and fraud risks in 2026.

Digital Transformation in Title Operations

Modern title companies increasingly employ artificial intelligence to accelerate title searches, analyze risk patterns, and identify potential fraud. These systems review decades of records in hours rather than days, reducing costs and improving accuracy.

Blockchain technology presents intriguing possibilities for property records management. Some jurisdictions experiment with distributed ledger systems that could create immutable ownership records, potentially simplifying future title searches. However, implementation challenges and regulatory hurdles suggest widespread adoption remains years away.

Electronic closings gained momentum during the COVID-19 pandemic, allowing parties to complete transactions remotely. This shift accelerated industry modernization, though fully digital processes still face legal and practical obstacles in many states. The evolution parallels transformations in other financial sectors, from electronic trading platforms to digital banking services.

Emerging Risks and Coverage Adaptations

Contemporary title insurance faces new challenges unknown to earlier generations. Cybersecurity threats now endanger closing transactions, with criminals intercepting wire transfers or creating fraudulent documents using sophisticated technology. Enhanced policies increasingly address cyber-related title fraud, reflecting evolving risk landscapes.

Climate change also influences title insurance considerations. Properties in flood-prone areas may face access restrictions or structural requirements affecting marketability. While traditional policies don't cover environmental risks directly, these factors influence underwriting decisions and property values.

Investment and Financial Analysis Perspectives

For investors analyzing the title insurance sector, several factors merit consideration. The industry's defensive characteristics provide relative stability during economic volatility, though growth correlates strongly with transaction volumes.

Sector Performance Metrics

Key indicators for evaluating title insurance companies include:

- Combined ratio: Loss and expense ratios relative to premium revenue

- Market share: Competitive positioning within target regions

- Technology investment: Capacity for operational efficiency gains

- Regulatory compliance: Ability to navigate varied state requirements

Understanding these metrics alongside broader financial analysis concepts enables comprehensive sector evaluation. The industry typically maintains favorable loss ratios compared to property-casualty insurance, given the preventive nature of pre-closing title examinations.

Major publicly traded companies in the sector include First American Financial Corporation, Old Republic International, Fidelity National Financial, and Stewart Information Services. Their performance reflects both real estate market conditions and operational efficiency improvements.

Historical Patterns and Future Outlook

Reviewing long-term industry data reveals cyclical patterns tied to housing markets and interest rate environments. Low rates typically stimulate both purchase activity and refinancing, driving premium growth. Rising rates initially dampen refinancing but may eventually support premiums through sustained purchase activity if employment and income growth remain healthy.

The relationship between title insurance premiums and broader economic indicators offers valuable analytical insights. Premium volumes often lead housing price trends by several quarters, providing forward-looking signals about market direction. For those studying market patterns and historical precedents, these connections illuminate complex relationships between real estate finance and economic cycles.

Demographic trends also influence long-term industry prospects. Millennials entering peak homebuying years suggest sustained transaction volumes, while aging baby boomers may downsize or relocate. Understanding these dynamics helps project future industry performance and identify emerging opportunities.

Title insurance represents a critical component of real estate finance, protecting ownership rights against historical defects while adapting to contemporary challenges. By examining this industry through both current operations and historical evolution, investors and analysts gain deeper understanding of risk management innovation and market dynamics. Historic Financial News provides the tools to explore these connections, offering interactive charts and AI-powered analysis that reveal patterns across market cycles and help users learn from past real estate and financial market movements.