Private Equity Guide: Strategies and Insights for 2025

As global markets shift and uncertainty rises, private equity stands at the forefront of financial innovation in 2025. Its influence continues to expand, shaping investment opportunities and redefining value creation across industries.

This guide offers a comprehensive look into private equity, providing strategies, trends, and actionable insights for investors, fund managers, and professionals. Whether you are new to the field or a seasoned expert, you will find up-to-date knowledge on core principles, advanced tactics, regulatory changes, and emerging prospects.

Explore the essentials of private equity, uncover key investment strategies, and stay ahead of evolving market dynamics. Ready to discover new opportunities and maximize your impact? Dive deeper into the world of private equity with us.

Understanding Private Equity: Fundamentals and Market Overview

Private equity stands as a pivotal force in global finance, shaping businesses and investment portfolios alike. To navigate this evolving landscape, it is crucial to understand the fundamentals, fund types, key players, operational mechanics, and prevailing market trends. Let us break down the essential building blocks of private equity for 2025.

Defining Private Equity

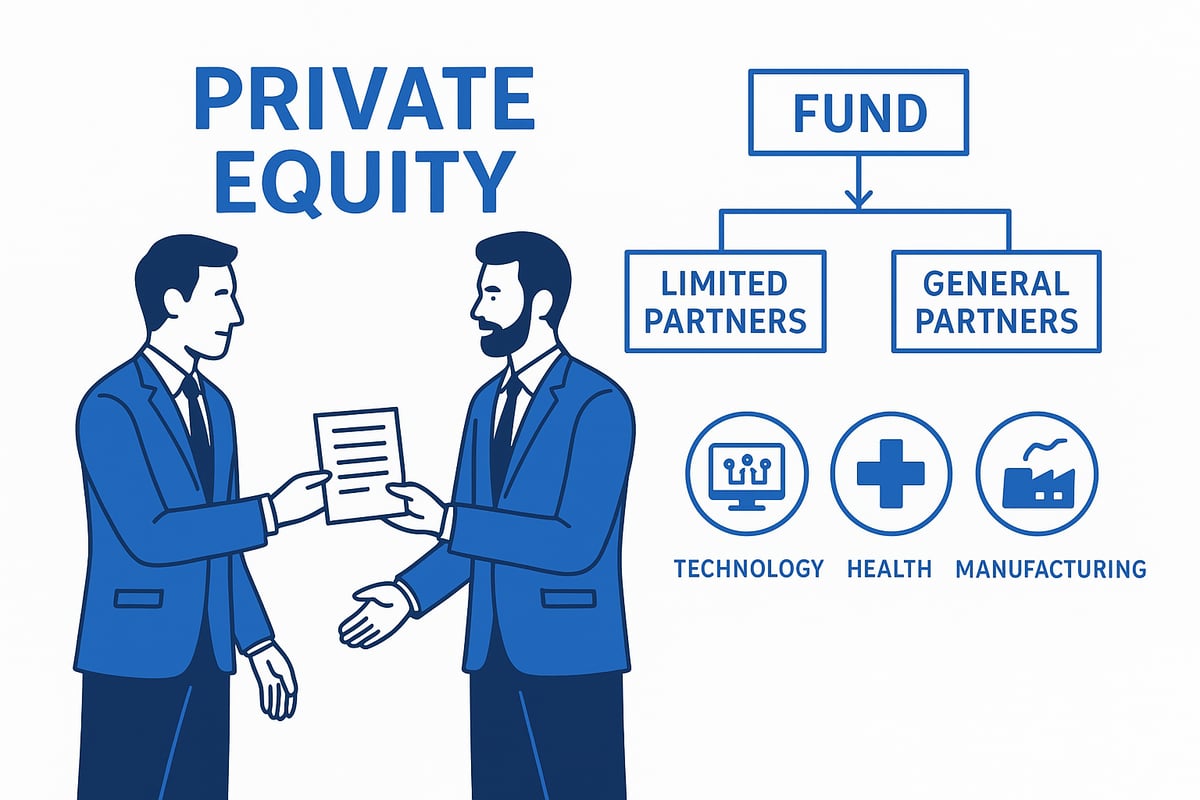

Private equity refers to pooled investment capital that targets non-public companies or takes public firms private. Unlike public market investments, private equity typically involves direct ownership and a hands-on approach to value creation. Fund structures often use limited partnerships, with general partners managing investments and limited partners providing most of the capital.

Investment horizons for private equity usually span 7 to 10 years, reflecting the time needed to unlock value. According to Preqin, the industry surpassed $7 trillion globally in 2023. One of the main advantages is the illiquidity premium, offering potentially higher returns in exchange for longer lock-up periods and less frequent liquidity. Understanding what is paid-in capital is essential, as it defines investor commitments and the capital available for investments.

Types of Private Equity Funds

Private equity encompasses a range of fund types, each with specific objectives and risk profiles. The most common strategies include:

- Buyout funds, which acquire controlling stakes, often using leverage

- Growth capital funds, supporting expansion in mature firms

- Venture capital, backing early-stage and innovative startups

- Mezzanine funds, providing hybrid debt-equity financing

- Distressed asset funds, targeting underperforming companies

Leveraged buyouts remain the dominant transaction, while funds may opt for minority or majority investments. Some focus on specific sectors, such as technology or healthcare, while others diversify across industries.

Key Players in Private Equity

The private equity ecosystem is driven by several key participants. Leading private equity firms—such as Blackstone, KKR, and Carlyle—manage large portfolios and set industry benchmarks. Limited partners (LPs) provide the bulk of capital; these include pension funds, endowments, sovereign wealth funds, and high-net-worth individuals.

Fund managers and specialized advisors play a critical role in sourcing deals, conducting due diligence, and overseeing portfolio companies. Notably, institutional investors contributed over 60 percent of new private equity capital in 2024, highlighting their influence and commitment to the asset class.

How Private Equity Funds Operate

Private equity funds follow a structured lifecycle. The process begins with fundraising, where managers seek capital commitments from investors. Once the fund is established, investment teams source and screen potential deals, applying rigorous due diligence to identify attractive opportunities.

Value creation is a cornerstone of private equity, achieved through operational improvements, management changes, and strategic repositioning. Exit strategies are diverse, including initial public offerings, secondary sales, trade sales, and recapitalizations. Each stage aims to maximize returns for both general and limited partners.

Recent Performance and Market Trends

Recent years have seen private equity outperform public markets, with average net internal rates of return (IRRs) between 15 and 18 percent in 2022 and 2023. The sector faces increasing competition, fueled by record levels of dry powder and a surge in deal activity.

Regional dynamics are shifting, with Asia-Pacific and Europe gaining prominence. Technology and healthcare deals have accelerated, particularly since the pandemic. As private equity continues to evolve, keeping pace with these trends is essential for investors and professionals seeking to capitalize on new opportunities.

Core Private Equity Strategies for 2025

The landscape of private equity in 2025 is defined by innovation, adaptability, and a diverse mix of investment approaches. As investors seek returns amid evolving market dynamics, understanding core private equity strategies is essential. Each strategy offers unique advantages, risk profiles, and opportunities for value creation.

Leveraged Buyouts (LBOs)

Leveraged buyouts remain a cornerstone of private equity strategy in 2025. LBOs involve acquiring a company primarily using borrowed funds, allowing firms to take control with limited upfront capital. The acquired company's assets often serve as collateral for the debt.

A classic example is KKR’s LBO of a manufacturing firm in 2023, which highlighted the strategic use of high leverage. Typical debt-to-equity ratios can range significantly, influencing both risk and return. For an in-depth look at this metric, see Debt-to-equity ratio explained.

LBOs accounted for about 40 percent of global private equity deal volume in 2024. While offering the potential for outsized returns, they require careful financial structuring and operational expertise to manage risk.

Growth Capital Investments

Growth capital investments are designed for businesses seeking expansion without relinquishing majority control. This private equity strategy targets mature companies with strong growth potential, especially in technology, healthcare, and emerging markets.

In these deals, private equity firms often provide funding for product rollouts, market entry, or acquisitions. A notable trend is the surge in growth equity for SaaS companies, as digital transformation accelerates.

Minority and majority growth deals coexist, giving flexibility in risk-sharing and governance. The appeal of growth capital lies in its ability to fuel expansion while aligning with the company’s long-term vision.

Venture Capital and Early-Stage Investing

Private equity firms are increasingly active in late-stage venture capital, supporting startups in sectors such as fintech, biotech, and AI. This crossover approach allows private equity to participate in the innovation cycle and access high-growth opportunities.

Record levels of VC dry powder, exceeding 300 billion dollars in 2024, have intensified competition for promising startups. Exit pathways include IPOs and strategic sales, offering potential for significant returns.

The integration of private equity and venture investing reflects a trend toward diversification and adaptability, as firms seek exposure to disruptive technologies and scalable business models.

Distressed and Special Situations

Distressed and special situations investing focuses on underperforming or financially troubled companies. Private equity firms deploy capital and operational expertise to restructure, turn around, or reposition these businesses.

Post-pandemic, private equity played a pivotal role in retail restructurings, demonstrating the value of strategic intervention. These investments carry higher risk but can deliver substantial returns if turnaround efforts succeed.

Strategies include operational restructuring, management changes, and cost optimization. For investors with a high risk tolerance, distressed investing offers unique access to undervalued assets.

Secondary Market Strategies

The secondary market has become a vital component of private equity, providing liquidity for investors and flexibility for managers. This strategy involves buying and selling existing interests in private equity funds, known as LP secondaries, as well as GP-led continuation funds.

In 2023, secondary market volume reached 130 billion dollars, reflecting strong demand for liquidity solutions. GP-led transactions and continuation vehicles are increasingly common, enabling firms to hold high-performing assets longer.

Secondary strategies help private equity participants manage portfolio risk, rebalance allocations, and access new opportunities without direct primary commitments.

Sector-Specific and Thematic Investing

Sector-specific and thematic investing is gaining traction in private equity as firms seek to capitalize on industry trends and long-term themes. Focus areas include renewable energy, healthcare, technology, and ESG-driven strategies.

The rise of climate-focused funds in 2024 exemplifies this shift, with ESG-themed private equity funds growing by 20 percent year over year. Thematic investing enables firms to align with investor demand for sustainable and responsible capital deployment.

By targeting sectors with strong tailwinds, private equity managers can generate differentiated returns and respond to evolving market dynamics.

Co-Investments and Direct Investments

Co-investments and direct investments offer limited partners (LPs) the opportunity to invest alongside general partners (GPs) in specific deals. This private equity approach provides benefits such as lower fees, increased transparency, and greater control over deal selection.

Pension funds and institutional investors are allocating more capital to co-investments, seeking alignment of interests and enhanced returns. However, these deals require robust due diligence and clear governance structures.

Co-investment strategies strengthen relationships between LPs and GPs, while offering a tailored approach to portfolio construction within private equity.

Key Trends and Opportunities in Private Equity for 2025

The private equity landscape in 2025 is rapidly evolving, offering both seasoned professionals and new entrants a variety of opportunities and challenges. As technology advances, sustainability becomes a priority, and global dynamics shift, understanding the latest trends is crucial for success in private equity. This section explores the most significant developments shaping the industry, from digital innovation to macroeconomic impacts.

Digital Transformation and Technology Enablement

Digital transformation is at the core of private equity strategies in 2025. Firms are increasingly leveraging artificial intelligence, advanced analytics, and automation to enhance deal sourcing, due diligence, and portfolio management. AI-driven insights help identify promising targets and accelerate value creation. Notably, 35% of new private equity deals in 2024 involved tech-enabled companies, underscoring the sector’s shift toward digital-first business models. For a deeper analysis of these and other themes, see 2025 private equity trends.

PE-backed platforms in sectors like digital health and fintech are becoming more common. As technology reshapes industries, private equity investors who embrace digital tools gain a competitive edge. The integration of data-driven strategies is no longer optional but essential for sustained growth.

ESG and Sustainable Investing

Environmental, social, and governance (ESG) factors are now central to private equity investment decisions. Limited partners increasingly demand robust ESG integration, pushing firms to adopt sustainability metrics and impact-driven strategies. Regulatory frameworks in the US and EU require greater transparency, amplifying the focus on responsible investing.

Blackstone’s launch of a $1B ESG-focused fund in 2024 exemplifies this trend. Private equity managers are not just seeking returns but also positive societal outcomes. ESG-themed funds grew 20% year over year, reflecting a market-wide shift. Investors who prioritize ESG are better positioned to attract capital and manage long-term risks.

Globalization and Emerging Markets

Private equity is becoming more global, with significant activity shifting toward Asia-Pacific, Latin America, and Africa. These regions offer attractive growth rates, expanding consumer markets, and less-saturated deal environments. In 2024, emerging markets accounted for 25% of new private equity funds raised.

Cross-border transactions are rising, but they bring currency and regulatory risks. Southeast Asia, for instance, saw a surge in private equity investments targeting technology and infrastructure. Firms that adapt to local market dynamics and build strong regional networks can unlock new value creation opportunities.

Fundraising and Capital Flows

Despite global uncertainty, private equity fundraising remains robust. Global dry powder reached a record $2.5 trillion, giving firms ample capital to deploy. However, fundraising is increasingly concentrated among large, established managers, while niche and specialized funds are gaining traction with targeted strategies.

Higher interest rates present challenges, leading some investors to favor mega-funds with proven track records over newer entrants. The choice between broad diversification and sector specialization is shaping capital flows. Understanding investor preferences is vital for successful fundraising in today’s private equity market.

Competition and Valuation Pressures

Competition for quality deals is intensifying in private equity, leading to higher valuations and compressed returns. Strategic buyers, special purpose acquisition companies (SPACs), and family offices are all active in the deal market, driving up median EBITDA multiples for buyouts to 11x in 2024.

To maintain strong performance, private equity firms are focusing on sourcing proprietary deals and employing creative structuring. Increased competition requires disciplined underwriting and a proactive approach to value creation. Navigating these pressures is essential for achieving target returns.

Innovation in Fund Structures and Liquidity Solutions

Private equity is witnessing innovation in fund structures, designed to enhance flexibility and liquidity for investors. Evergreen funds, continuation vehicles, and net asset value (NAV) financing are gaining popularity. The secondary market also provides liquidity solutions, with secondary market volume hitting $130 billion in 2023.

GP-led secondary transactions and continuation funds accounted for 15% of secondary volume, reflecting demand for new ways to manage portfolio duration and exits. These innovations help private equity adapt to changing investor needs and market cycles, offering more options for capital deployment and realization.

Impact of Macroeconomic Factors

Macroeconomic conditions are influencing private equity strategies and outcomes in 2025. Interest rates, inflation, and geopolitical risks affect deal financing, valuations, and exit timelines. For example, sector focus has shifted in response to supply chain disruptions and regional instability.

Exit activity slowed in 2024, with average holding periods increasing to six years. Private equity investors must stay agile, adapting to evolving economic conditions and regulatory environments. Those who anticipate macroeconomic shifts can better manage risk and seize emerging opportunities.

Navigating Risks and Due Diligence in Private Equity

Navigating the complexities of private equity requires a clear understanding of the risks, rigorous due diligence, and proactive portfolio management. Investors and fund managers must balance return potential with prudent risk controls, especially in a rapidly evolving financial environment.

Risk Factors in Private Equity Investing

Private equity investing offers attractive returns, but it comes with unique risks. Illiquidity is a primary concern, as capital is often locked for 7 to 10 years. The use of leverage, especially in buyouts, increases financial risk and can amplify losses during downturns.

Market cycles and macroeconomic shocks, such as rising interest rates or geopolitical instability, can impact portfolio performance. According to Private Equity Trends in 2025, 20% of private equity funds underperformed public benchmarks between 2022 and 2024. Understanding these factors is crucial for effective risk management.

Due Diligence Best Practices

Thorough due diligence is the foundation of successful private equity investing. This process involves commercial, financial, legal, and operational analysis of target companies. Advanced analytics and technology are increasingly used to identify hidden risks and validate assumptions.

Enhanced ESG due diligence is now standard, as investors demand accountability on environmental and social issues. Red flag identification, such as undisclosed liabilities or weak management teams, helps mitigate downside risk. Comprehensive due diligence protects capital and supports better investment decisions in private equity.

Value Creation and Portfolio Management

Active value creation is a hallmark of private equity. Firms drive performance through operational improvements, such as cost reduction, revenue growth initiatives, and digital transformation. Upgrading leadership and implementing best practices can unlock additional value.

Portfolio management also focuses on risk monitoring and strategic adjustments. For example, private equity managers often optimize supply chains and leverage technology to boost efficiency. Well-executed value creation plans are central to achieving superior returns and managing risks.

Exit Strategies and Timing

Successful exits are essential for realizing gains in private equity. Common strategies include IPOs, trade sales, secondary buyouts, and recapitalizations. Market conditions and timing play a significant role in determining exit options and valuations.

In recent years, delayed IPOs due to market volatility have affected exit timelines. For instance, 2024 saw a 15% drop in private equity-backed IPOs and an increase in average holding periods to 6 years. Careful planning and flexibility are required to maximize exit outcomes.

Aligning Interests and Managing Conflicts

Effective alignment of interests is crucial in private equity partnerships. Fee structures, such as management fees and carried interest, must be transparent and fair. Co-investment opportunities allow limited partners to participate directly in deals, fostering greater alignment.

Managing conflicts of interest requires strong governance and clear communication. Regulatory scrutiny on fee disclosures is increasing, prompting firms to enhance transparency. By prioritizing alignment, private equity managers can build trust and support long-term success.

Regulatory and Tax Considerations in Private Equity for 2025

Understanding the regulatory and tax environment is crucial for anyone navigating the private equity landscape in 2025. As the industry evolves, new rules and heightened scrutiny shape how funds operate, raise capital, and deliver returns. Staying current on these developments can help protect investments and uncover new opportunities.

Evolving Regulatory Landscape

The private equity sector faces a rapidly shifting regulatory landscape in 2025. Regulators, especially in the US and EU, have intensified oversight, requiring more detailed disclosures and transparency from fund managers. New SEC rules on fund disclosures, introduced in 2024, demand greater clarity on fees, performance, and conflicts of interest.

Many private equity professionals are adjusting fund structures and compliance systems to meet these standards. According to 2025 Private Equity Predictions, these regulatory changes are expected to impact both fundraising and deal execution, increasing compliance costs and operational complexity. For global managers, adapting to varied international requirements remains a top priority.

Taxation of Private Equity Investments

Tax considerations remain central for private equity funds and their investors. The debate over carried interest tax treatment continues, with policymakers in the US and UK considering reforms that could affect after-tax returns. Fund managers must also navigate the Base Erosion and Profit Shifting (BEPS) framework, which has introduced new cross-border tax rules.

Private equity managers are reviewing fund domiciles and deal structures to optimize tax efficiency. Changes in tax regimes may require funds to reconsider how profits are distributed and reported. As the landscape evolves, proactive tax planning is essential to maintain compliance and maximize investor value.

Transparency, Reporting, and Investor Protection

Transparency is now a defining feature of private equity investing. Enhanced disclosure requirements, such as Europe’s Sustainable Finance Disclosure Regulation (SFDR) and updated US Form PF rules, are designed to protect investors and ensure fair practices.

Investors increasingly demand clear reporting on fees, performance, and ESG metrics. According to a recent Preqin survey, 70% of limited partners cite transparency as their top concern. Fund managers are responding by upgrading reporting systems and providing more frequent, detailed updates to stakeholders.

Ethical and Social Impact Debates

Ethical issues are shaping the dialogue around private equity in 2025. Critics often point to job losses, aggressive cost-cutting, and short-term priorities driven by some private equity strategies. The sector’s role in sensitive industries, such as healthcare and housing, is under close public and regulatory scrutiny.

Calls for responsible investing and stakeholder engagement are growing louder. Many private equity firms are adopting ESG frameworks and committing to more balanced, long-term value creation. The debate over private equity’s social impact is likely to intensify, pushing the industry to evolve and address broader stakeholder needs.

Expert Insights and Outlook for Private Equity in 2025

As private equity continues to evolve in 2025, expert perspectives shed light on the strategies, innovations, and market shifts that will define the year ahead. In this section, we share leading industry views, highlight transformative technologies, explore new opportunities for entrants, and examine the importance of historical lessons for navigating future cycles.

Leading Industry Perspectives

Industry leaders expect private equity to remain resilient despite macroeconomic headwinds. Top fund managers and institutional investors forecast robust deal activity, especially in sectors like infrastructure, private credit, and technology. Blackstone and other major players emphasize the importance of flexible capital allocation and sector rotation as market conditions shift.

A key trend is the continued rise of continuation funds and secondary transactions, providing liquidity and longer holding periods for quality assets. For a comprehensive view of these themes, see Global M&A trends in private capital: 2025 outlook. Experts also note that disciplined valuation and rigorous due diligence are critical as competition intensifies and deal multiples remain elevated.

Innovations Shaping the Future

Technological advancements are redefining private equity operations. Firms are increasingly leveraging AI and data analytics to enhance deal sourcing, due diligence, and portfolio management. Machine learning models help identify patterns and opportunities that were previously difficult to spot, leading to more informed investment decisions.

Blockchain technology is also gaining traction for fund administration, enabling greater transparency and efficiency in reporting. The adoption of generative AI tools has begun to automate labor-intensive tasks such as document review and compliance checks. These innovations are expected to drive operational excellence and create new sources of value within private equity portfolios.

Opportunities for New Entrants and Niche Players

The private equity landscape in 2025 is opening up to a broader range of participants. Specialized funds focusing on climate tech, healthcare innovation, and fintech are attracting significant investor interest. Emerging managers and micro-PE funds are leveraging unique strategies to access niche markets and underserved sectors.

Lower barriers to entry, including access to co-investment opportunities and innovative fund structures, are encouraging entrepreneurial fund managers to launch new vehicles. Search funds and sector-specific strategies are gaining momentum, allowing new entrants to carve out distinct positions in the competitive private equity ecosystem.

Preparing for the Next Cycle

Learning from past market cycles remains essential for success in private equity. Industry veterans point to lessons from the dot-com bubble, the global financial crisis, and the COVID-19 pandemic as reminders of the importance of adaptability and risk management. Funds with flexible mandates and diversified portfolios have historically outperformed peers during downturns.

As interest rates, geopolitical risks, and market volatility persist, experts advise maintaining a disciplined approach to capital deployment and exit planning. Resilience, agility, and a long-term perspective will be key as private equity firms navigate the next phase of industry growth and transformation.

As you’ve seen throughout this guide, understanding private equity’s evolving strategies and market dynamics is key to navigating 2025’s opportunities and risks. But to truly grasp the patterns shaping private equity—and the broader financial landscape—you need more than just current headlines. Imagine exploring interactive historical data, uncovering connections, and learning from the past to make smarter moves today. If you’re ready to see the bigger picture and become part of a platform built for curious, forward-thinking investors like you, Join Our Beta and help us bring financial history to life.