LIBOR: The Rise, Fall, and Legacy of a Benchmark Rate

The London Interbank Offered Rate, commonly known as LIBOR, served as the foundational benchmark interest rate for global financial markets from 1986 until its gradual discontinuation between 2021 and 2023. This reference rate influenced an estimated $300 trillion in financial contracts worldwide at its peak, affecting everything from mortgages and student loans to complex derivatives and commercial paper. Understanding the story of LIBOR provides crucial insights into how benchmark rates shape financial markets, the consequences of rate manipulation, and the challenges of transitioning massive financial systems to new standards. For anyone studying historical market events, LIBOR represents a fascinating case study in institutional failure, regulatory reform, and market adaptation.

The Origins and Mechanics of LIBOR

LIBOR emerged in the 1980s as London established itself as a dominant global financial center. The British Bankers' Association (BBA) formalized the rate in 1986 to create a standardized benchmark for interbank lending costs. Before LIBOR, banks struggled with inconsistent pricing mechanisms for loans and derivatives, creating inefficiencies across international markets.

The calculation methodology appeared straightforward on the surface. Each business day, a panel of major banks submitted estimates of their borrowing costs across multiple currencies and loan durations. The BBA would collect these submissions, remove the highest and lowest quartiles, and average the remaining figures to produce the daily LIBOR rate. This process occurred for five currencies (U.S. Dollar, Euro, British Pound, Japanese Yen, and Swiss Franc) across seven different maturity dates ranging from overnight to one year.

Currency and Tenor Structure

| Currency | Number of Tenors | Most Common Use Cases |

|---|---|---|

| U.S. Dollar | 7 | Adjustable-rate mortgages, corporate loans |

| Euro | 7 | European derivatives, cross-currency swaps |

| British Pound | 7 | UK mortgages, sterling-denominated bonds |

| Japanese Yen | 7 | Asian market derivatives, trade finance |

| Swiss Franc | 7 | Private banking, wealth management products |

The three-month U.S. Dollar LIBOR became the most widely referenced rate globally. Financial institutions used this tenor as a floating rate basis for countless agreements, making it integral to pricing decisions across the financial ecosystem.

The Golden Era of Market Dominance

Throughout the 1990s and early 2000s, LIBOR cemented its position as the world's most important benchmark rate. The rate's widespread adoption created powerful network effects. As more institutions referenced LIBOR in their contracts, it became increasingly impractical to use alternative benchmarks. This self-reinforcing cycle elevated LIBOR from a useful reference point to an indispensable component of global finance.

Financial innovation during this period heavily relied on LIBOR as a foundation. Interest rate derivatives, including swaps and futures contracts, used the benchmark to determine payment obligations between counterparties. Corporate treasurers structured debt agreements with interest payments tied to LIBOR plus a credit spread measured in basis points. Even retail financial products like adjustable-rate mortgages in the United States frequently referenced the rate.

The benchmark's flexibility contributed to its popularity. Unlike fixed rates, LIBOR-based instruments could adjust to changing market conditions, theoretically providing fair pricing for both borrowers and lenders. This characteristic made the rate particularly valuable for long-term contracts where interest rate environments might shift substantially over time.

- Derivatives contracts: Over-the-counter interest rate swaps totaling hundreds of trillions in notional value

- Corporate lending: Syndicated loans and revolving credit facilities for multinational corporations

- Structured products: Asset-backed securities and collateralized debt obligations

- Consumer finance: Adjustable-rate mortgages, home equity lines of credit, student loans

- Municipal finance: Variable-rate demand obligations issued by state and local governments

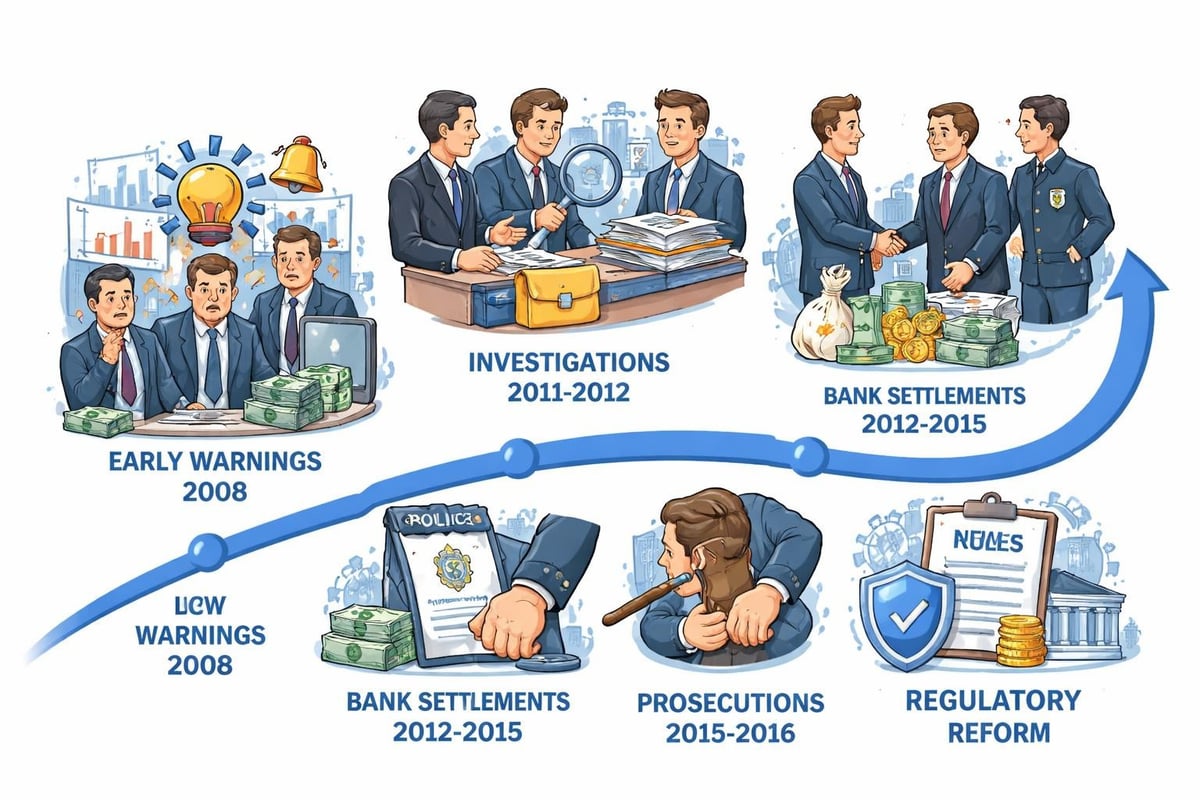

The Scandal That Shook Global Markets

The 2008 financial crisis exposed fundamental weaknesses in the LIBOR system. As credit markets froze, actual interbank lending became scarce, making rate submissions increasingly hypothetical rather than based on real transactions. This environment created opportunities for manipulation that several major banks exploited for profit.

Investigations beginning in 2012 revealed systematic fraud spanning multiple years. Traders at institutions including Barclays, UBS, and Royal Bank of Scotland had colluded to manipulate LIBOR submissions to benefit their derivatives positions. Some manipulations aimed to make individual banks appear healthier during the financial crisis by submitting artificially low borrowing cost estimates. Other instances involved coordinated efforts to move rates in directions favorable to trading desks.

Major LIBOR Manipulation Settlements

| Institution | Settlement Amount | Year | Primary Regulator |

|---|---|---|---|

| Barclays | $453 million | 2012 | U.S. DOJ, UK FSA, CFTC |

| UBS | $1.5 billion | 2012 | Multiple agencies |

| Royal Bank of Scotland | $612 million | 2013 | U.S. DOJ, CFTC |

| Rabobank | $1 billion | 2013 | U.S. DOJ, CFTC |

| Deutsche Bank | $2.5 billion | 2015 | Multiple agencies |

The scandal's impact extended far beyond financial penalties. Criminal prosecutions resulted in prison sentences for individual traders, a rare outcome in financial regulation. Public trust in financial benchmarks evaporated, forcing regulators worldwide to confront the systemic vulnerabilities of rates based primarily on expert judgment rather than observable transactions. The Financial Stability Board began coordinating international efforts to reform benchmark rate practices.

Regulatory Response and Reform Initiatives

Authorities recognized that LIBOR's fundamental design created perverse incentives. The methodology relied on subjective estimates from a relatively small panel of banks, many of which held trading positions sensitive to rate movements. This structure combined insufficient transaction data with conflicts of interest, creating conditions ripe for abuse.

The UK Financial Conduct Authority (FCA) assumed regulatory oversight of LIBOR in 2013, transferring responsibility from the British Bankers' Association to the Intercontinental Exchange Benchmark Administration (IBA). The IBA implemented enhanced governance protocols, including stricter submission standards and surveillance mechanisms. However, these reforms couldn't address the more fundamental problem: declining interbank lending meant LIBOR increasingly lacked the transaction volume needed for a robust benchmark.

By 2017, the FCA announced that LIBOR would be phased out by the end of 2021. This decision reflected recognition that mandating banks to submit estimates for a dying market represented an untenable long-term solution. The FDIC highlighted concerns about the rate's reliability and the systemic risks of maintaining a benchmark without adequate underlying transactions.

Regulators worldwide coordinated the development of alternative reference rates (ARRs) designed to avoid LIBOR's flaws. These replacement benchmarks shared several common principles:

- Transaction-based calculation: Rates derived from actual market transactions rather than estimated borrowing costs

- Deep, liquid markets: Underlying markets with sufficient trading volume to resist manipulation

- Transparent methodology: Clear, reproducible calculation processes published regularly

- Robust governance: Independent administrators with comprehensive oversight frameworks

- Regulatory supervision: Direct regulatory oversight to ensure integrity and reliability

The Transition to Alternative Reference Rates

Different jurisdictions developed replacement benchmarks tailored to their specific financial markets. The United States adopted the Secured Overnight Financing Rate (SOFR), which the Federal Reserve Bank of New York calculates based on overnight Treasury repurchase agreement transactions. The SOFR methodology reflects actual borrowing costs in a market with approximately $1 trillion in daily transaction volume, providing robustness that LIBOR lacked.

Europe transitioned to the Euro Short-Term Rate (€STR), while the United Kingdom introduced the Sterling Overnight Index Average (SONIA) reformed version. Japan implemented the Tokyo Overnight Average Rate (TONAR), and Switzerland adopted the Swiss Average Rate Overnight (SARON). Each alternative reflected similar transaction-based principles while accommodating local market structures.

The transition process presented enormous operational challenges. Financial institutions needed to identify LIBOR-linked contracts, many buried in decades-old documentation. Legal teams wrestled with fallback language that specified what would happen if LIBOR ceased to exist. The Office of Financial Research tracked implementation progress across various market segments, highlighting the complexity of converting trillions in existing contracts.

Key Differences Between LIBOR and SOFR

| Characteristic | LIBOR | SOFR |

|---|---|---|

| Calculation basis | Bank estimates | Actual transactions |

| Market depth | Limited interbank lending | $1 trillion daily repo market |

| Credit risk component | Includes bank credit risk | Risk-free (secured by Treasuries) |

| Forward-looking terms | Available | Developed later through derivatives |

| Currency coverage | Five currencies | U.S. Dollar only |

One significant challenge involved the structural differences between LIBOR and its replacements. LIBOR incorporated bank credit risk and term structure, while overnight rates like SOFR represented risk-free borrowing costs for a single day. This meant SOFR-based loans required credit adjustments to compensate lenders appropriately. Industry groups developed spread adjustments to maintain economic equivalence during the transition.

Market Impact and Legacy Contracts

The official cessation dates arrived in stages. Most LIBOR settings permanently stopped publication after June 30, 2023, though some U.S. Dollar settings continued temporarily in synthetic form to support legacy contracts. The comprehensive history of LIBOR demonstrates how a benchmark rate can become so deeply embedded in financial infrastructure that unwinding it requires years of coordinated effort.

Legacy contracts represented a persistent challenge. Some agreements lacked adequate fallback provisions, creating legal ambiguity about appropriate replacement rates. Legislative bodies in various jurisdictions passed laws establishing statutory replacements for tough legacy contracts that couldn't be amended through negotiation. The Government Finance Officers Association provided guidance to help state and local governments navigate the transition, recognizing the particular challenges facing public sector entities with limited resources.

Market participants learned valuable lessons about benchmark design and governance. The LIBOR experience demonstrated that widely-used financial benchmarks represent critical infrastructure requiring robust oversight. The transition also highlighted the importance of contract flexibility, as agreements lacking clear fallback provisions created unnecessary friction during the change process.

Financial institutions invested billions in systems updates, legal reviews, and contract renegotiations. Smaller market participants, including regional banks and municipal issuers, faced disproportionate challenges due to limited technical resources. Industry organizations developed tools and best practices to facilitate adoption, recognizing that successful transition required collective action across the entire financial ecosystem.

Lasting Implications for Financial Markets

The LIBOR story offers profound insights for anyone studying financial market evolution. The benchmark's four-decade journey from innovative solution to manipulated rate to obsolete reference demonstrates how market infrastructure must adapt to changing conditions. The manipulation scandal exposed how conflicts of interest and inadequate governance can corrupt essential market mechanisms, while the transition illustrated the challenges of coordinating change across globally interconnected financial systems.

For modern market participants, understanding LIBOR provides context for evaluating current benchmark rates. The principles underlying alternative reference rates-transaction-based calculation, transparent methodologies, robust governance-emerged directly from LIBOR's failures. Investors analyzing historical data must account for the benchmark transition when comparing yields, spreads, and other rate-sensitive metrics across different time periods.

The regulatory framework governing financial benchmarks strengthened considerably in LIBOR's aftermath. International coordination through bodies like the Financial Stability Board established baseline standards for benchmark administration. National regulators gained expanded authority to supervise critical reference rates, reducing the likelihood of similar manipulation occurring in successor benchmarks.

Students of financial history can observe how institutional inertia complicated necessary reforms. Despite clear evidence of LIBOR's problems emerging during the 2008 crisis, the transition didn't begin in earnest until nearly a decade later. This delay reflected the enormous coordination challenges inherent in changing deeply embedded market infrastructure, as well as the difficulty of building consensus among diverse stakeholders with competing interests.

The development of alternative rates demonstrates financial innovation responding to market needs. Overnight rates like SOFR initially seemed inadequate for replacing LIBOR's term structure, but derivatives markets developed forward-looking term rates that addressed this gap. This evolution shows how market participants can develop solutions to technical challenges when proper incentives align.

Lessons for Benchmark Rate Design

Financial market infrastructure requires continuous evaluation and improvement. The LIBOR experience highlighted several critical design principles for benchmark rates that remain relevant in 2026:

- Sufficient underlying activity: Benchmarks must rest on deep, liquid markets with robust transaction volumes

- Minimal conflicts of interest: Separating rate submission from proprietary trading reduces manipulation incentives

- Independent administration: Benchmark calculation should occur through entities without vested interests in rate levels

- Regulatory oversight: Direct supervision ensures compliance with governance standards and market integrity

- Transparent methodology: Clear, reproducible calculation processes enable market participants to verify accuracy

- Contingency planning: Contracts must include well-defined fallback provisions anticipating benchmark discontinuation

These principles apply beyond interest rate benchmarks to other critical market references. Commodity indices, currency benchmarks, and volatility measures all benefit from similar governance frameworks. Market participants evaluating reliance on any benchmark should assess whether these design elements are present.

The historical record shows that even widely-adopted financial infrastructure can require replacement when fundamental flaws emerge. Institutions must balance the benefits of standardization against the risks of excessive dependence on potentially vulnerable systems. Diversifying across multiple benchmarks or developing internal alternatives provides resilience against benchmark disruption.

The rise and fall of LIBOR represents one of the most significant transitions in modern financial history, offering timeless lessons about market structure, governance, and the challenges of coordinating change across global systems. Whether you're researching the 2012 manipulation scandal, analyzing the impact of benchmark transitions on historical portfolios, or studying regulatory responses to market failures, Historic Financial News provides the interactive tools and contextual analysis to understand how benchmark rates shaped decades of market activity and what their evolution reveals about financial market development.