Corporate Bonds: A Historical Analysis of Market Evolution

Corporate bonds have served as a cornerstone of capital markets for over a century, enabling companies to finance expansion, operations, and strategic initiatives while offering investors predictable income streams. From the railroad boom of the early 1900s to the complex debt instruments of modern markets, these securities have evolved alongside economic transformations, regulatory reforms, and technological innovations. Understanding the historical trajectory of corporate bonds reveals not only how companies have financed growth but also how investors have navigated risk, return, and market volatility across different economic eras. This historical perspective provides essential context for analyzing current market conditions and anticipating future trends.

The Foundation of Corporate Bond Markets

The modern corporate bond market emerged during the industrial expansion of the late 19th and early 20th centuries. Railroad companies pioneered the widespread use of bonds to finance infrastructure development, establishing patterns that other industries would follow for decades.

Early market characteristics included:

- Limited standardization across issuances

- Minimal regulatory oversight

- Heavy reliance on investment banker reputation

- Regional market fragmentation

- Direct negotiation between issuers and large investors

During this period, underwriters played a crucial role in connecting corporate issuers with wealthy individuals and institutional investors. The absence of formal credit rating systems meant that investor relationships and banker reputations served as the primary mechanisms for assessing creditworthiness. This relational approach to bond markets created significant information asymmetries between insiders and outside investors.

The Panic of 1907 and subsequent banking crises exposed vulnerabilities in this informal system, prompting calls for greater transparency and standardization. By the 1920s, the market had grown substantially, with utility companies, manufacturers, and retailers joining railroads as major issuers. However, the lack of comprehensive disclosure requirements and credit assessment standards would contribute to the devastating bond defaults of the Great Depression.

Credit Ratings and Market Development

The introduction of systematic credit ratings fundamentally transformed corporate bond markets. John Moody published the first publicly available bond ratings in 1909, followed by competitors Poor's, Standard Statistics, and Fitch in subsequent decades. Moody's credit rating system established categories that remain recognizable today, from high-grade investment securities to speculative bonds.

The Rating System Impact

Credit ratings addressed a critical market failure by providing standardized risk assessments accessible to all investors. This democratization of credit analysis enabled broader participation in bond markets and facilitated price discovery across thousands of issuances.

| Rating Category | Historical Default Rates (1920-1940) | Post-War Period (1950-1980) | Modern Era (1990-2025) |

|---|---|---|---|

| AAA/Aaa | 0.5% | 0.2% | 0.1% |

| A/Baa | 3.2% | 1.8% | 1.2% |

| Below Investment Grade | 18.5% | 12.3% | 8.7% |

The Great Depression tested rating agency credibility as thousands of bonds defaulted despite previously favorable ratings. This experience led to increased scrutiny of rating methodologies and eventually contributed to regulatory reforms. The Securities Act of 1933 and Securities Exchange Act of 1934 established disclosure requirements that complemented rating agency assessments, creating a dual system of market transparency.

Following World War II, the corporate bond market expanded dramatically as American corporations financed domestic expansion and international operations. Investment-grade bonds became staples of institutional portfolios, while pension funds and insurance companies emerged as dominant buyers. This institutional demand drove standardization of bond features, including maturity dates, coupon structures, and sinking fund provisions.

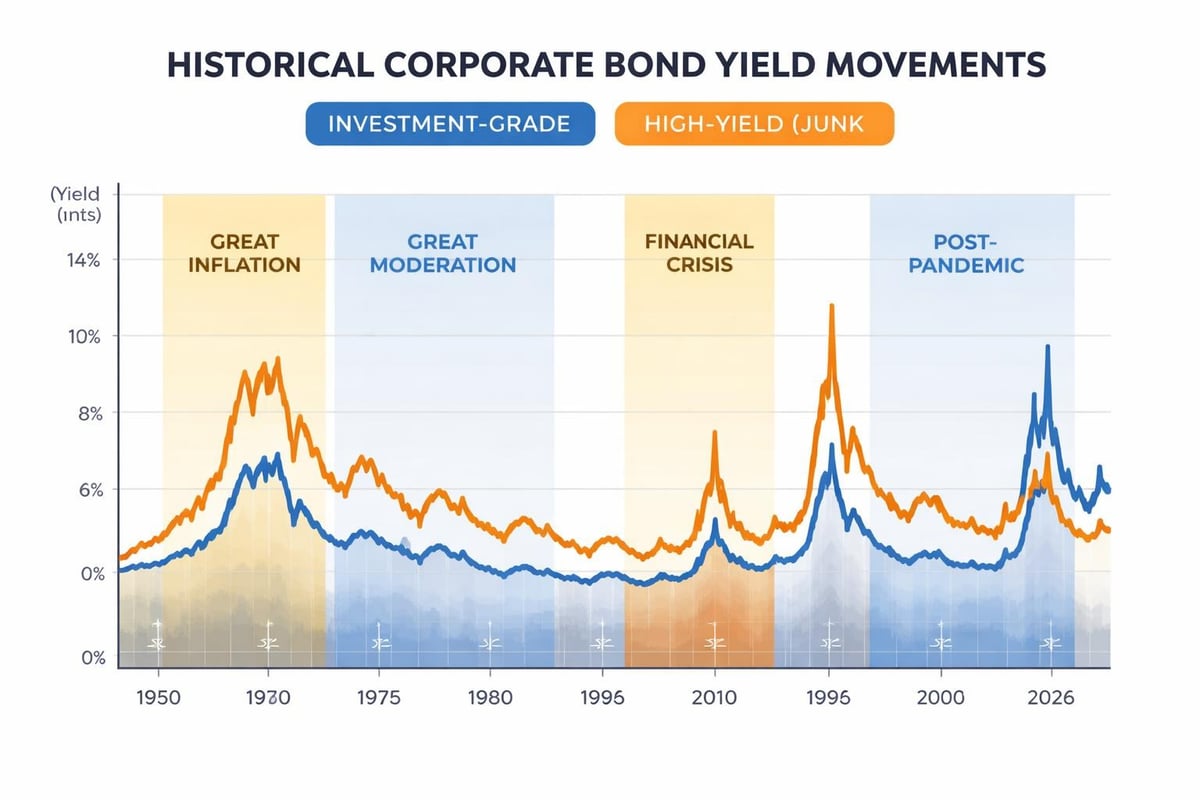

Yield Dynamics Through Economic Cycles

Corporate bond yields have fluctuated dramatically across economic cycles, reflecting changing inflation expectations, monetary policy regimes, and credit risk perceptions. Analyzing these patterns reveals how macroeconomic conditions shape fixed-income returns.

During the 1950s and early 1960s, investment-grade corporate bonds typically yielded between 3% and 5%, with spreads over government securities remaining relatively stable. This benign environment reflected low inflation, steady economic growth, and minimal default risk among established issuers. The measured differences in basis points between different credit qualities remained compressed.

The High Inflation Era

The inflationary spiral of the 1970s fundamentally disrupted bond markets. As inflation exceeded 10% annually, nominal yields on corporate bonds surged to unprecedented levels. By 1981, high-grade corporate bonds yielded over 15%, while lower-rated securities offered yields exceeding 18%. These elevated yields reflected both inflation compensation and increased default risk as economic volatility intensified.

Key factors driving 1970s-1980s yield volatility:

- Federal Reserve monetary policy shifts

- Oil price shocks and supply disruptions

- Currency market instability

- Rising corporate leverage ratios

- Regulatory changes affecting financial institutions

The Volcker Federal Reserve's inflation-fighting campaign of the early 1980s created severe stress for corporate borrowers. High interest rates increased debt service costs while simultaneously weakening economic demand. Default rates climbed, particularly among heavily leveraged industrial companies and real estate firms. This period demonstrated how corporate bonds amplify macroeconomic risks through both direct interest rate exposure and indirect effects on issuer creditworthiness.

The High-Yield Revolution

The emergence of the high-yield bond market in the 1980s represented one of the most significant innovations in corporate finance history. While bonds rated below investment grade had existed previously, they primarily resulted from "fallen angels" that had been downgraded after issuance. Michael Milken and Drexel Burnham Lambert pioneered the original issuance of high-yield bonds, creating a market for companies that lacked investment-grade credit profiles.

This innovation enabled smaller companies, leveraged buyouts, and growth firms to access bond markets that had previously been limited to established blue-chip corporations. The high-yield market grew from less than $10 billion in outstanding securities in 1980 to over $200 billion by 1989. This expansion fundamentally altered corporate capital structures and competitive dynamics across industries.

However, the high-yield boom also produced excesses. Default rates among speculative-grade bonds exceeded 10% annually in 1990-1991, causing significant losses for investors who had underestimated credit risk. The collapse of Drexel Burnham Lambert in 1990 and subsequent investigations raised questions about market practices and conflicts of interest in underwriting and distribution.

Market Maturation and Lessons

Despite these challenges, the high-yield market matured through the 1990s and 2000s. Improved credit analysis, better understanding of recovery rates, and portfolio diversification strategies enabled institutional investors to incorporate speculative-grade bonds systematically. Historical corporate bond data shows that risk-adjusted returns on diversified high-yield portfolios often exceeded investment-grade alternatives over long time horizons.

| Period | Average High-Yield Returns | Investment-Grade Returns | Default Rate |

|---|---|---|---|

| 1985-1995 | 11.2% | 8.7% | 4.8% |

| 1996-2006 | 8.9% | 6.4% | 3.2% |

| 2007-2017 | 7.6% | 5.1% | 3.9% |

| 2018-2025 | 6.2% | 4.3% | 2.8% |

Financial Crisis and Regulatory Response

The 2008 financial crisis severely stressed corporate bond markets. Credit spreads widened dramatically as investors fled to government securities, with investment-grade spreads exceeding 600 basis points and high-yield spreads surpassing 2,000 basis points at the crisis peak. This represented the most severe disruption since the Great Depression.

The crisis revealed critical vulnerabilities in market structure and credit assessment. Rating agencies faced intense criticism for assigning investment-grade ratings to asset-backed securities that subsequently defaulted. The concentration of ownership and opacity of over-the-counter trading contributed to liquidity challenges that amplified price volatility.

Post-crisis reforms included:

- Enhanced disclosure requirements under Dodd-Frank regulations

- Mandatory reporting of corporate bond transactions through TRACE

- Revised rating agency oversight and liability provisions

- Capital requirements for financial institutions holding corporate bonds

- Stress testing incorporating corporate credit scenarios

These reforms improved market transparency and reduced some systemic risks. FINRA's corporate bond trading data now provides comprehensive transaction information that was unavailable before the crisis. This transparency has enhanced price discovery and enabled more sophisticated market analysis.

The Federal Reserve's intervention through quantitative easing programs also fundamentally altered corporate bond markets. By purchasing investment-grade bonds and providing liquidity support, the Fed compressed credit spreads and lowered borrowing costs. This support enabled a massive expansion of corporate debt issuance through the 2010s, with outstanding corporate bonds exceeding $10 trillion by 2020.

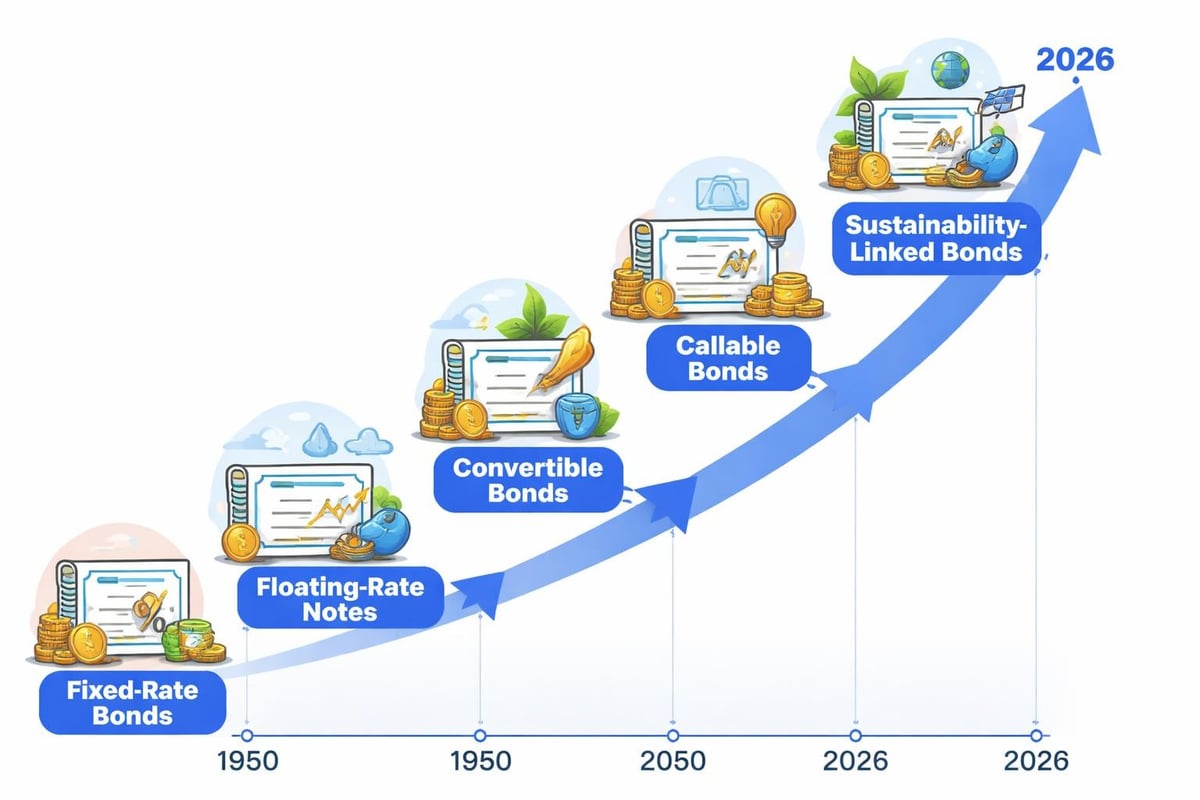

Evolution of Bond Structures and Features

Corporate bond structures have evolved substantially to meet changing issuer needs and investor preferences. While traditional fixed-rate bonds with standard face value and maturity provisions remain common, markets have developed numerous variations.

Convertible bonds gained popularity during the technology boom of the 1990s, offering investors equity upside participation while providing issuers with lower coupon costs. These hybrid securities appealed particularly to growth companies whose uncertain cash flows made traditional fixed obligations less attractive. The convertible market has experienced multiple cycles of expansion and contraction, with issuance volumes highly sensitive to equity market valuations and volatility.

Floating-rate notes emerged as solutions to interest rate uncertainty, with coupons adjusting based on reference rates such as LIBOR or SOFR. These instruments shift interest rate risk from issuers to investors, making them attractive during periods of rising rates. The transition from LIBOR to alternative reference rates in the early 2020s represented a significant operational challenge for markets, requiring repricing of trillions in outstanding securities.

Specialized Instruments and Market Segments

Sustainability-linked bonds and green bonds represent recent innovations, with issuance growing from minimal levels in 2015 to over $500 billion annually by 2025. These instruments tie financial terms to environmental, social, or governance metrics, reflecting changing investor priorities and corporate commitments. While initially concentrated among European issuers, American corporations have increasingly accessed this market segment.

The international dimension of corporate bonds has also expanded dramatically. American companies now routinely issue bonds in European and Asian markets, while foreign corporations access U.S. dollar bond markets. This globalization has created arbitrage opportunities, increased competition among underwriters, and complicated regulatory oversight across jurisdictions.

Market Structure and Technology Transformation

Corporate bond trading has transitioned from relationship-based telephone negotiations to electronic platforms incorporating algorithmic pricing and execution. This transformation has reduced transaction costs, improved price transparency, and enabled broader market participation.

However, corporate bonds remain predominantly traded over-the-counter rather than on organized exchanges. This structure reflects the diversity of bond characteristics, with each issuance having unique features regarding maturity, coupon, covenants, and embedded options. The fragmentation across thousands of individual securities limits the standardization necessary for exchange trading.

Modern market infrastructure components:

- Electronic trading platforms connecting multiple dealers

- Data aggregation services providing comprehensive pricing information

- Index construction methodology for benchmark development

- Risk analytics incorporating scenario analysis and stress testing

- Regulatory reporting systems ensuring transaction transparency

Research on corporate bond markets continues to examine how market structure affects liquidity, price efficiency, and capital allocation. Historical analysis reveals that market microstructure has significant implications for issuer costs and investor returns, with periods of structural transition often generating trading opportunities and risks.

The rise of passive investing through bond index funds and exchange-traded funds has also reshaped markets. These vehicles now hold over $1.5 trillion in corporate bonds, creating persistent demand for index-eligible securities while potentially affecting relative valuations between indexed and non-indexed bonds.

Understanding the historical evolution of corporate bonds provides essential context for analyzing current market conditions and identifying patterns that may repeat or diverge in future cycles. From the informal markets of the early 1900s through the sophisticated electronic platforms of 2026, corporate bonds have continuously adapted to economic changes, regulatory reforms, and technological innovations. Historic Financial News offers investors, students, and market professionals the tools to explore these patterns through interactive historical charts, AI-powered analysis, and comprehensive coverage of market events that shaped corporate bond markets across more than a century of development.