Capital Loss: Understanding Tax Implications & Strategies

Understanding the concept of capital loss is fundamental for anyone navigating investment markets, whether you're analyzing historical trends or managing a contemporary portfolio. A capital loss occurs when you sell an asset for less than its purchase price, representing a negative return on investment. This seemingly simple concept carries significant implications for tax planning, portfolio strategy, and long-term wealth management. Throughout market history, investors have experienced capital losses during crashes, corrections, and individual stock declines, making this knowledge essential for informed decision-making.

What Constitutes a Capital Loss

A capital loss materializes when the sale price of a capital asset falls below its original cost basis. Capital assets include stocks, bonds, real estate, and other investment properties. The IRS provides detailed guidance on capital gains and losses, establishing clear rules for how these transactions affect your tax obligations.

Short-Term vs. Long-Term Capital Losses

The classification of capital loss depends on your holding period. Assets held for one year or less generate short-term capital losses, while those held longer produce long-term capital losses. This distinction matters significantly for tax purposes.

Key differences include:

- Short-term losses offset short-term gains first

- Long-term losses offset long-term gains initially

- Excess losses can offset the opposite category

- Different tax rates apply to gains in each category

Historical market events illustrate these principles vividly. During the 2008 financial crisis, investors who sold bank stocks after holding them for several years realized long-term capital losses, while day traders experienced short-term losses. Understanding fundamental analysis can help investors evaluate whether holding or selling makes strategic sense during market volatility.

Tax Treatment and Deduction Limits

The tax code treats capital loss with specific provisions designed to limit immediate deductions while providing long-term relief. For 2026, taxpayers can deduct up to $3,000 ($1,500 if married filing separately) of net capital loss against ordinary income annually.

| Loss Type | Annual Deduction Limit | Carryover Allowed |

|---|---|---|

| Short-term | $3,000 combined | Indefinite |

| Long-term | $3,000 combined | Indefinite |

| Combined excess | $3,000 total | Indefinite |

When total capital losses exceed capital gains plus the annual deduction limit, the excess carries forward to future tax years. Understanding loss carryovers becomes crucial for multi-year tax planning strategies.

Calculating Your Net Capital Loss

Determining your net position requires aggregating all capital transactions for the tax year:

- Calculate total short-term capital gains and losses

- Calculate total long-term capital gains and losses

- Net each category separately

- Combine the results to determine overall position

- Apply the $3,000 deduction limit if applicable

This systematic approach ensures accurate tax reporting. Nolo's guide on claiming stock loss deductions provides practical steps for proper documentation and filing.

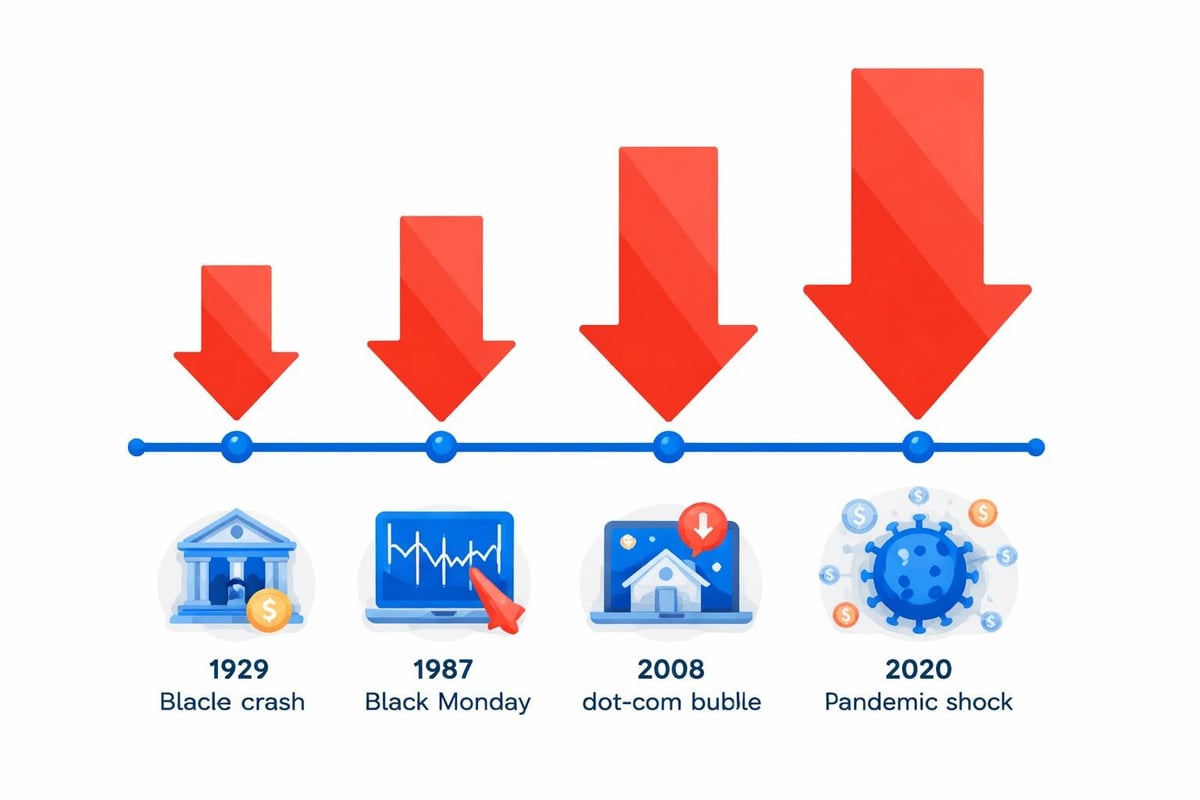

Historical Context: Capital Losses Through Market Cycles

Examining capital loss through historical market events reveals patterns that inform contemporary strategy. The Great Depression witnessed unprecedented capital losses as stock values plummeted 89% from peak to trough between 1929 and 1932. Investors who sold during the panic locked in devastating losses that took decades to recover.

Notable Market Downturns and Capital Loss Patterns

The Dot-Com Bubble (2000-2002): Technology stocks experienced severe declines, with the NASDAQ Composite falling approximately 78% from its peak. Investors who purchased at inflated valuations and sold during the crash realized substantial capital losses. Many carried these losses forward for years, offsetting gains from subsequent recovery periods.

The 2008 Financial Crisis: Financial sector stocks collapsed as the mortgage crisis unfolded. Major institutions saw share prices decline 80-90%, creating massive capital losses for shareholders. The crisis demonstrated how concentrated positions amplify loss potential, reinforcing diversification principles.

The 2020 Pandemic Shock: March 2020 brought a rapid 34% decline in major indices within weeks. Investors who panic-sold at the bottom experienced capital losses, while those who maintained positions through recovery avoided realizing losses. This event highlighted the importance of distinguishing between paper losses and actual realized capital loss.

Strategic Uses of Capital Loss

Sophisticated investors strategically harvest capital losses to optimize tax efficiency. Tax-loss harvesting involves selling investments at a loss to offset capital gains, reducing overall tax liability. This practice gained prominence following the introduction of modern capital gains taxation.

Tax-Loss Harvesting Methodology

Implementing effective tax-loss harvesting requires careful planning:

- Identify underperforming positions with unrealized losses

- Evaluate whether the investment thesis remains valid

- Consider replacement securities to maintain market exposure

- Monitor wash sale restrictions to ensure deduction validity

- Document transactions thoroughly for tax reporting

The wash sale rule prohibits claiming a capital loss deduction if you purchase substantially identical securities within 30 days before or after the sale. This rule prevents taxpayers from selling losing positions solely for tax benefits while immediately repurchasing them.

Carryover Provisions and Multi-Year Planning

When annual capital losses exceed the deduction limit, understanding carryover mechanics becomes essential. The Motley Fool's carryover calculation guide explains how to track and apply unused losses across tax years.

Carryover characteristics:

- No expiration date for carried losses

- Losses retain their short-term or long-term classification

- Apply in subsequent years using the same netting process

- Continue until fully utilized or taxpayer's death

| Tax Year | Net Capital Loss | Used Against Income | Carried Forward |

|---|---|---|---|

| 2024 | ($15,000) | ($3,000) | ($12,000) |

| 2025 | ($8,000) | ($3,000) | ($17,000) |

| 2026 | $25,000 gain | $25,000 offset | $0 |

This table illustrates how a taxpayer might utilize accumulated capital losses over multiple years, eventually offsetting a substantial gain without current-year tax liability.

Capital Loss and Portfolio Rebalancing

Beyond tax considerations, capital loss plays a vital role in portfolio management and rebalancing strategies. Recognizing when to realize losses requires balancing tax benefits against investment fundamentals.

Decision Framework for Realizing Losses

Fundamental deterioration: When a company's business prospects deteriorate permanently, realizing the capital loss and redeploying capital makes strategic sense. Historical examples include retailers that failed to adapt to e-commerce or energy companies disrupted by technological change.

Valuation reassessment: If market conditions reveal that initial purchase price reflected overvaluation rather than temporary market inefficiency, accepting the capital loss prevents further capital erosion. The value investing discipline emphasizes cutting losses when thesis invalidation occurs.

Portfolio rebalancing needs: Systematic rebalancing may trigger capital losses when reducing overweight positions. This disciplined approach maintains target allocations despite realizing losses on recently purchased positions.

Impact on Investment Returns and Rate of Return

Capital loss directly reduces investment rate of return, making accurate performance measurement essential. Total return calculations must account for both realized and unrealized losses.

Measuring True Investment Performance

Calculating returns with capital losses:

- Add all capital gains and income received during the period

- Subtract all realized capital losses from sales

- Account for unrealized losses on current holdings

- Divide net result by initial investment to determine percentage return

This methodology provides accurate performance assessment across market cycles. Historical analysis reveals that investors who panic-sold during downturns experienced permanent capital loss, while patient investors often recovered.

Regulatory Evolution and Capital Loss Treatment

The tax treatment of capital loss has evolved significantly since the modern income tax system's inception in 1913. Understanding this evolution provides context for current regulations and potential future changes.

Key historical developments:

- 1913: Original income tax law treated capital gains and losses as ordinary income

- 1921: First preferential capital gains tax rate introduced

- 1978: Holding period for long-term treatment reduced from one year to nine months, later adjusted to current one-year threshold

- 1986: Tax Reform Act temporarily eliminated preferential rates, treating gains as ordinary income

- 2003: Reduced rates for qualified dividends and long-term gains introduced

These changes demonstrate how policy shifts affect capital loss utility and investment strategy. Current capital gains tax rates for 2026 maintain preferential treatment for long-term positions.

Common Mistakes and Misconceptions

Investors frequently misunderstand capital loss applications, leading to suboptimal tax outcomes and strategy errors.

Frequent errors include:

- Ignoring wash sale restrictions when repurchasing similar securities

- Failing to track carryover amounts across tax years

- Misclassifying holding periods for short-term versus long-term treatment

- Overlooking state tax implications of capital transactions

- Neglecting to harvest losses in taxable accounts while holding gains

Questions about capital-loss harvesting and the wash sale rule frequently arise during tax season, highlighting the complexity investors face.

Integration with Broader Financial Planning

Capital loss considerations extend beyond immediate tax benefits into comprehensive wealth management. Estate planning, retirement account management, and cross-generational wealth transfer all intersect with capital loss treatment.

Estate Planning Implications

At death, capital assets receive a stepped-up basis to fair market value, eliminating unrealized capital losses. This creates planning considerations:

| Strategy | Benefit | Consideration |

|---|---|---|

| Harvest losses before death | Utilize tax deductions | Requires liquidity needs assessment |

| Gift appreciated assets | Avoid capital gains | Recipient receives carryover basis |

| Hold losses in taxable accounts | Preserve deduction opportunity | Monitor overall portfolio allocation |

Understanding how capital loss interacts with estate planning helps optimize multi-generational wealth transfer while maximizing tax efficiency.

Sector-Specific Capital Loss Patterns

Historical analysis reveals that certain sectors experience capital losses more frequently due to industry dynamics. Technology, retail, and energy sectors show higher volatility and loss frequency compared to utilities or consumer staples.

Technology sector characteristics:

- Rapid innovation creates obsolescence risk

- Winner-take-all dynamics magnify losses for second-tier competitors

- Valuation compression during market corrections hits growth stocks hardest

- Historical examples include typewriter manufacturers, floppy disk producers, and failed social networks

Energy sector patterns:

- Commodity price cycles drive periodic capital losses

- Regulatory shifts create stranded asset risks

- Technological disruption threatens traditional business models

- Oil price crashes historically generated widespread capital losses

Studying these patterns through platforms like Historic Financial News helps investors recognize recurring dynamics and adjust strategies accordingly.

Record-Keeping and Documentation Requirements

Proper documentation ensures you can substantiate capital loss deductions if audited. The IRS requires specific information for each transaction.

Essential records include:

- Purchase date and price for each security

- Sale date and proceeds received

- Brokerage statements confirming transactions

- Adjusted basis calculations for corporate actions

- Carryover worksheets from previous years

Maintaining organized records simplifies annual tax preparation and provides audit protection. Many investors use portfolio management software to track cost basis automatically, reducing manual calculation requirements.

Future Outlook and Policy Considerations

As of 2026, discussions continue regarding potential tax code modifications that could affect capital loss treatment. Proposed changes include adjusting deduction limits, modifying holding period requirements, or eliminating preferential rates for capital gains.

Potential policy directions:

- Increasing the annual deduction limit above $3,000

- Implementing mark-to-market taxation for certain assets

- Expanding or restricting wash sale rule applications

- Harmonizing state and federal capital loss treatments

Staying informed about legislative developments helps investors adapt strategies to changing regulatory environments. Historical precedent shows that tax policy shifts create both challenges and opportunities for strategic capital loss management.

Understanding capital loss mechanics empowers investors to make informed decisions during market volatility while optimizing tax efficiency across multiple years. By examining how investors navigated losses during historical market events, you gain perspective on effective strategies and common pitfalls. Historic Financial News provides the historical context and analytical tools to explore how capital losses shaped market outcomes across different eras, helping you recognize patterns and apply lessons from past market cycles to contemporary investment decisions.